Your orders are finally moving. A few local customers found you on Instagram, then a few more started to reorder, and now you're packing boxes at the kitchen table or coordinating with a small fulfillment partner while trying to answer customer emails before dinner. It feels good. It also changes the stakes fast.

If you sell coffee, skincare, wellness goods, pet products, seasonings, or packaged food online, the risk isn't abstract. One damaged shipment, one customer reaction, one charge dispute, or one coverage gap with a 3PL can turn a great month into a stressful one. That's why e commerce insurance matters. Not because you're expecting disaster, but because you're building something worth protecting.

Table of Contents

- Start with general liability

- When a BOP fits better

- Coverage that becomes more important as operations spread out

- The 3PL handoff is where many brands get surprised

- Product complaints are rarely simple

- Digital risk still belongs to physical-goods brands

- Marketplace rules change by channel

- Marketplace Insurance Requirements at a Glance

- What sellers of physical goods should do before a platform asks

- What to prepare before you ask for quotes

- What to ask the agent

- What usually works and what usually doesn't

Your Brand Is Growing So Are the Risks

The first time you get a burst of orders, your brain usually splits in two. One half is thrilled. The other half starts asking practical questions. What happens if a package disappears? What if a customer says your balm irritated their skin? What if your labels say one thing, but a buyer claims they understood something else?

That shift is normal. It means you're no longer treating your brand like a hobby. You're treating it like a business with real products, real customers, and real exposure.

For makers selling physical goods, the risk lives in the handoff points. You make the product. A carrier handles the package. A marketplace processes the order. A customer opens the box and uses the item in a way you can't control. Insurance steps in so one bad outcome doesn't pull your attention away from product quality, customer care, and growth.

Growth changes what you need to protect

When you only sell a few orders a month, it's easy to assume you can absorb problems as they come. That usually works until the problem is bigger than expected. A claim doesn't have to be dramatic to be expensive. It just has to involve the wrong timing, the wrong customer, or the wrong gap in your coverage.

The professional move isn't waiting until something goes wrong. It's putting coverage in place while your brand still has room to choose carefully.

The broader insurance market is moving in the same direction. The global Property and Casualty insurance market that supports online seller protections is projected to grow at an annual rate of +4.7% up to 2026, reflecting the need to cover cyber liability, product liability, and shipping errors for digital sellers, according to Allianz's global insurance outlook.

Peace of mind is operational

Good coverage doesn't make you fearful. It makes you calmer. You stop making every shipping delay feel personal. You stop wondering whether one complaint could derail your month. You build with more confidence because the business has structure behind it.

If you're getting serious about selling online, selling on Loyaltie fits that same mindset. It gives independent brands a marketplace where people discover and buy directly from the maker, with no middleman between your product story and the customer.

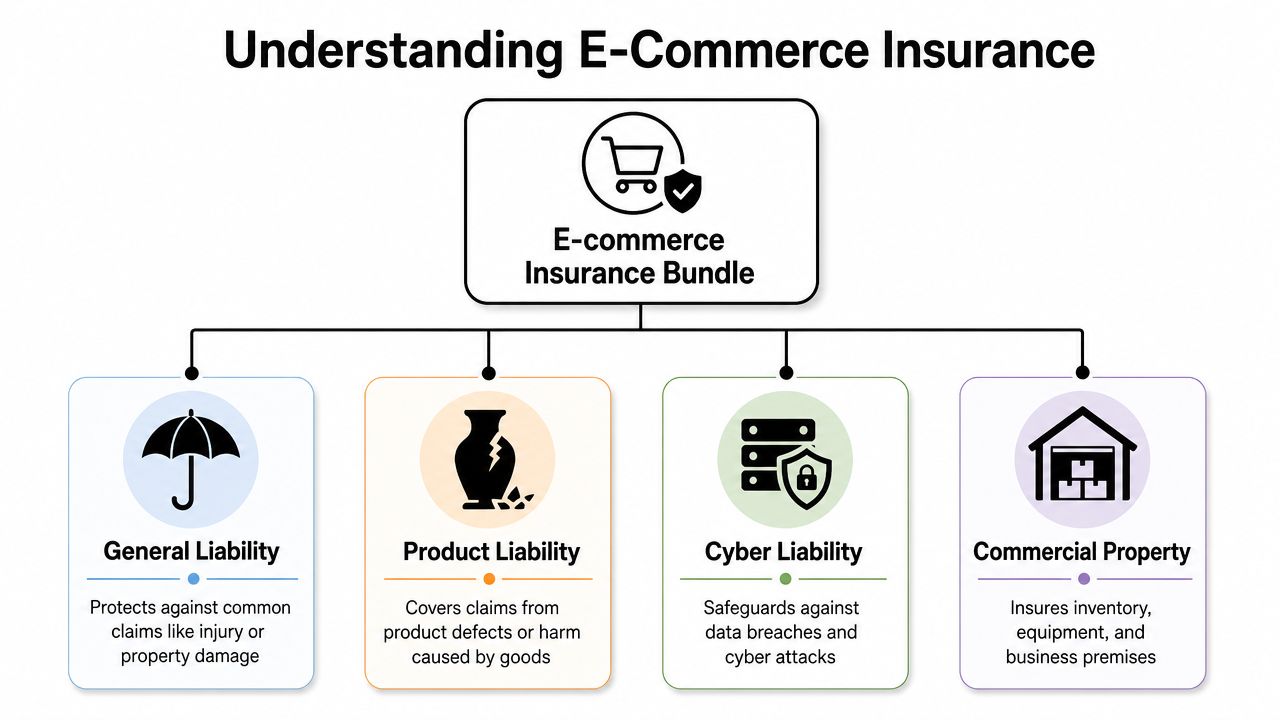

What E-Commerce Insurance Actually Is

A lot of founders ask for “e commerce insurance” as if it's one boxed product sitting on a shelf. It usually isn't. For most makers, it's a bundle of policies that works together.

That distinction matters because a seasoning brand, a skincare line, and a supplement seller don't carry the same exposures. They may all sell online, but what can go wrong is different. The right setup protects the actual way your business runs, not the label on the category.

Think in layers not in one policy

The cleanest way to understand this is to think in layers.

General liability is your everyday safety net. It handles common third-party injury or property damage claims tied to business operations.

Product liability is the shield around what you sell. If a buyer says your product caused harm or damaged property, this is the part of the program designed for that exposure.

Cyber insurance protects the digital side. If you collect customer data, process payments, or run your store through online systems, you have data risk even if you never touch a physical storefront.

Commercial property helps protect inventory, equipment, and spaces used for the business, depending on how and where those assets are listed.

Practical rule: If your business takes payments online and ships physical goods, you have both digital risk and product risk. Treating only one side leaves a hole.

Why coordinated coverage works better

The brands that handle risk well don't buy random policies one at a time without a plan. They coordinate them. That's especially important when a single event creates more than one kind of problem. A hacked admin login can interrupt orders and expose customer data. A product complaint can lead to legal costs and marketplace trouble. A warehouse issue can become both an inventory problem and a fulfillment problem.

As Vouch explains in its guide for online sellers, e commerce insurance works best as a coordinated program, not a single policy, often integrating Technology Errors & Omissions, Cyber Insurance, and Product Liability for direct-to-consumer brands facing transaction failures and data breach risks.

What this means for makers

If you make food, wellness products, or skincare, don't ask for a vague “online store policy” and hope the agent fills in the blanks. Start with what you sell, where inventory sits, how orders ship, and what customer data you hold. That's how you end up with protection that matches the business you operate.

The Most Common Policies for Independent Makers

Policy shopping gets easier once you sort your risks by what can hurt the business first. For independent makers selling physical goods online, that usually means starting with claims tied to the product itself, then protecting the inventory, tools, and shipments that keep orders going out.

Start with general liability

For many new sellers, Commercial General Liability, or CGL, is the first policy to price. It covers core third-party claims such as bodily injury, property damage, and legal defense costs. For makers of food, skincare, wellness products, candles, or pet goods, that matters because the claim often starts after the item leaves your hands.

A customer does not need to prove you were careless before a complaint becomes expensive. Skin irritation, an ingredient sensitivity, a labeling dispute, or damage to someone else's property can trigger a claim. If you use ingredients with allergen, fragrance, supplement, or topical exposure, ask the broker to confirm exactly how product liability is handled and whether any ingredients or product categories are excluded.

A practical example is Habanero Salt-Free All-Purpose Seasoning Blend, Garlic & Onion, Everyday No-Sodium Flavor, Net Weight 2.25 ozShaker Bott | DSLW Seasonings by Loyaltie. It is a packaged pantry item with straightforward use. Even so, packaged food can raise questions about ingredient statements, cross-contact, spoilage, or how a customer interprets the label.

When a BOP fits better

A Business Owner's Policy, or BOP, often makes more sense once you have inventory and equipment worth protecting. It usually combines general liability with commercial property coverage in one policy, which can be cleaner and sometimes less expensive than piecing those coverages together separately.

This setup tends to work well for brands with one main operating location and a predictable workflow, such as a home studio, small production space, or rented commercial unit. It can cover finished stock, raw materials, packaging, label printers, mixers, shelving, and laptops, but only if those items and locations are described correctly in the application.

That detail matters. If you keep part of your stock at home, part at a shared kitchen, and overflow inventory with a fulfillment partner, a standard quote built around one address can leave gaps.

Coverage that becomes more important as operations spread out

Growth changes the insurance mix. The policy that looked fine at 50 orders a month can be thin once you add wholesale accounts, a 3PL, staff logins, and recurring ingredient purchases from multiple suppliers.

The next policies to review usually include:

- Cyber insurance: Useful if you store customer data, rely on apps and integrations, or want help with breach response and recovery costs.

- Inland marine or transit coverage: Important if inventory travels to pop-ups, retailers, co-packers, or fulfillment centers.

- Product recall or contamination-related coverage: Worth discussing for food, supplements, and some topical products where one batch issue can create disposal, notice, and replacement costs.

- Higher-risk product endorsements: Sometimes needed for products with stronger claim exposure, such as ingestibles, essential-oil blends, or formulas with active ingredients.

If you collect customer emails, shipping details, or account information through your storefront, pair your insurance review with a clear privacy policy for your online store. Insurance can help with the cost of a cyber incident. It does not replace the basic legal and operational work of telling customers how you handle their data.

One more practical point. Ask who is responsible for loss at each handoff, especially if a 3PL receives, stores, picks, and ships your products. Your policy may cover part of that chain, the warehouse may carry its own insurance, and the carrier may limit what it pays. Those are separate promises, not one blanket answer.

For a grounded view of prevention and claims planning, review this expert advice on NJ business risks. The best policy stack is the one that matches how your brand makes, stores, and ships product, not the one that looks tidy on a generic quote.

Real-World Risks You Might Not Have Considered

Most generic insurance advice talks about slips, falls, and lawsuits in broad terms. Makers selling food, wellness products, skincare, and pet goods online face more specific trouble spots. The tricky part is that the riskiest moments often happen between locations, systems, and partners.

The 3PL handoff is where many brands get surprised

You've packed inventory, sent it to a fulfillment partner, and assumed your property coverage follows it. Sometimes it doesn't. That's the problem.

A key gap for makers is stock-in-transit and off-site inventory handled by a 3PL. Standard policies may exclude goods stored away from the listed location or leave confusion during the handoff window. Deshret Capital notes that 68% of e-commerce theft occurs in transit, which is exactly why this blind spot hurts brands that depend on shipping and outsourced fulfillment. Their explanation of this coverage gap is laid out in this risk-rating overview for ecommerce businesses.

If your broker never asks where inventory sits between your workspace, a carrier, and a 3PL, the quote probably isn't specific enough.

For a wellness brand shipping glass bottles or a food brand moving perishable ingredients, that gap matters even more. Loss can happen while goods are being transferred, scanned, staged, or stored off-site.

Product complaints are rarely simple

A customer says your face oil caused a reaction. A pet owner says a chew upset their dog's stomach. A buyer claims a seasoning blend was mislabeled for their dietary needs. Even when you believe your process was sound, responding still takes time, paperwork, and sometimes legal help.

Policy wording and product descriptions matter. Vague descriptions tend to create friction in underwriting and claims. Specific ingredients, intended use, country of manufacture, and packaging details usually make coverage conversations cleaner.

Digital risk still belongs to physical-goods brands

A lot of makers think cyber risk is for software companies. It isn't. If you run checkout online, collect addresses, store email lists, or connect third-party apps to your storefront, you have digital exposure.

One practical habit is to compare your insurance setup with your privacy workflow. Your public policies, order handling, and customer data practices should line up. If you need a reference point for how an online marketplace presents those expectations, Loyaltie's privacy policy for sellers and shoppers is useful because it shows the kind of transparency customers now expect.

For a broader operational lens, especially if you want a grounded checklist around claims prevention and day-to-day exposure, Liberty Insurance Associates shares expert advice on NJ business risks that's worth reading even if your brand sells beyond one state.

A short explainer can make some of these exposures easier to think through:

Navigating Marketplace Insurance Requirements

A founder hits a sales milestone on Amazon, gets an insurance notice, and scrambles for a certificate in 48 hours. That rush usually leads to the wrong policy, the wrong named insured, or coverage that satisfies the platform but leaves the brand exposed.

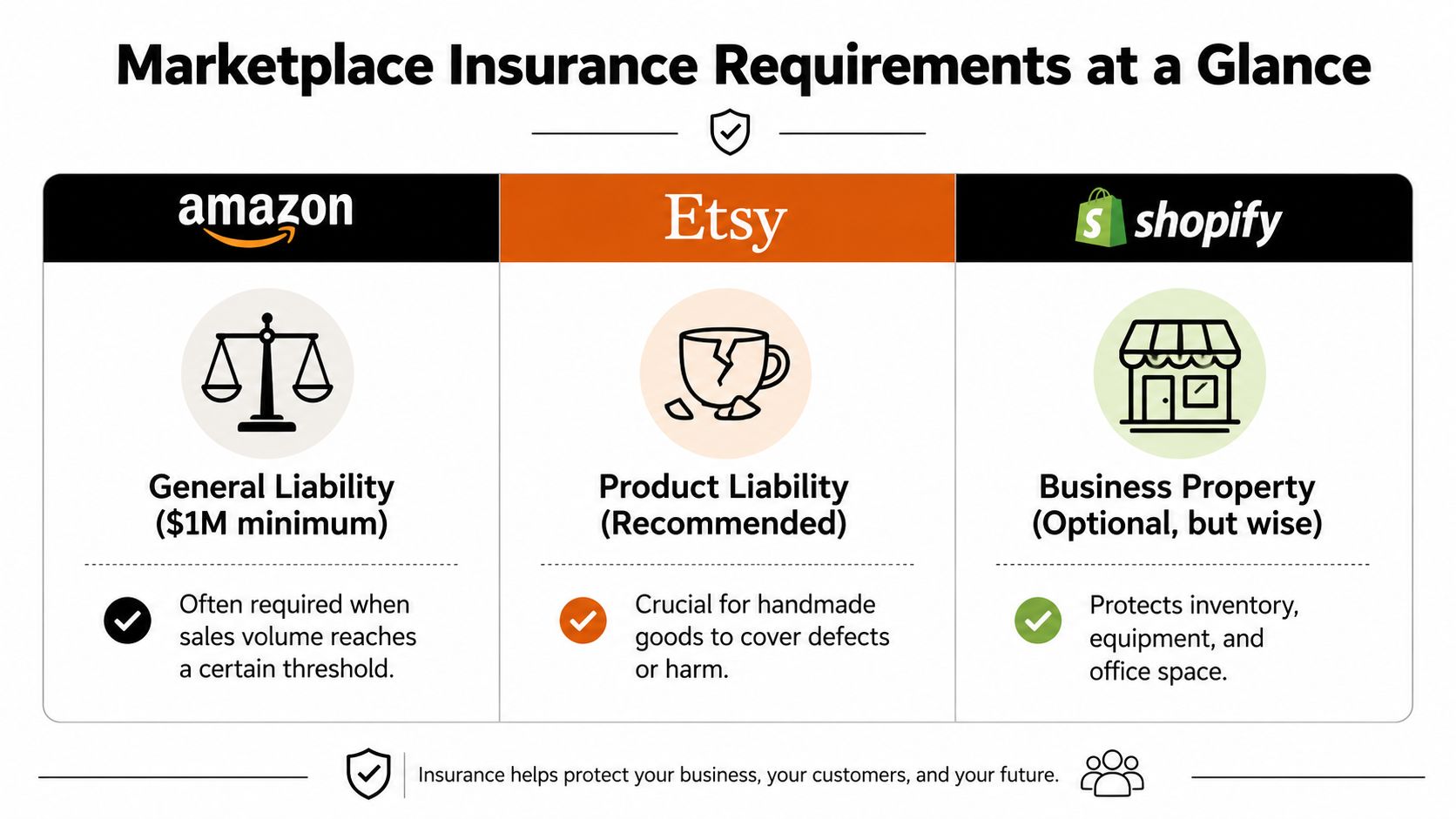

Marketplace rules change by channel

Each platform sets its own standards, and those standards can change without much warning. Amazon and Walmart tend to formalize insurance requirements once a seller reaches certain sales levels. Etsy and Shopify are usually quieter on formal insurance mandates, but a customer complaint about a reaction, a contamination issue, or a packaging injury still comes back to the seller.

That matters even more for independent makers in food, wellness, and skincare. Marketplaces care about proof of coverage. Your business also needs coverage that matches how your products are made, stored, labeled, and fulfilled.

Marketplace Insurance Requirements at a Glance

| Marketplace | Revenue Threshold for Requirement | Required Coverage Amount |

|---|---|---|

| Amazon | Sales threshold may trigger proof of insurance requirements | Commercial General Liability is commonly required |

| Walmart | Higher sales volume may trigger formal insurance review | Liability limits may be higher than other channels |

| Etsy | No widely stated standard requirement for many sellers | Seller still retains product liability exposure |

| Shopify | No platform-wide insurance requirement for many stores | Seller still retains product liability exposure |

A marketplace can help you get discovered. It does not take over liability for what you sell.

What sellers of physical goods should do before a platform asks

Start with the certificate details. Platforms often care about exact business names, entity structure, coverage dates, and insurer ratings. If your LLC name, DBA, and storefront name do not match cleanly, fix that before you upload anything.

Then look past the certificate. If you use a 3PL, confirm whether your policy covers stock at that location and whether the warehouse contract shifts any liability back to you. I have seen makers assume the fulfillment partner's policy protects their goods, only to learn it mainly protects the warehouse.

Ingredient-heavy products need another layer of attention. A general liability policy that looks fine for candles or mugs may be a poor fit for ingestibles, supplements, or leave-on skincare. Marketplaces rarely explain that distinction. They just ask for proof. The underwriting details are still your problem.

If you sell on multiple channels, keep one current insurance file with certificates, renewal dates, named additional insureds, and any platform-specific compliance notes. Loyaltie's seller resource library for growing online brands is a useful place to organize the operational side of that work alongside your sales channels.

Sellers dealing with transport and compliance issues on Amazon's logistics side can also learn from solving Amazon Relay insurance issues, which shows how exact these requirements can get once a platform is involved.

A Simple Checklist for Buying Your First Policy

The fastest way to waste money is to ask for “e commerce insurance” and stop there. That phrase is too broad to get you a useful quote. Progressive Commercial notes that 55% of sellers incorrectly believe a single e-commerce policy exists, when the better approach is a customized mix of General Liability, Product Liability, and Cyber coverage based on the business. Their explanation is in this guide to ecommerce insurance options.

What to prepare before you ask for quotes

Bring clean, specific information. Brokers can only match coverage to what they understand.

- What you sell: List exact product types, not fuzzy labels. “Salt-free seasoning blend” is more useful than “food products.” “Body oil with botanical ingredients” is more useful than “wellness.”

- Where inventory lives: Note whether goods are stored at home, in a studio, in a warehouse, or with a 3PL.

- How orders move: Say whether you ship yourself, use a fulfillment partner, or sell through marketplaces.

- What data you hold: Customer names, addresses, email lists, order history, payment flow, and any connected apps all matter.

What to ask the agent

Don't ask, “Do I need insurance?” Ask sharper questions.

- Does this quote include product liability by default?

- Are goods covered while in transit or at a 3PL?

- Is off-site inventory covered, and under what wording?

- What cyber events are included?

- Are there exclusions tied to ingredients, supplements, ingestibles, or topical products?

Buying tip: If the agent can't explain your exclusions in plain English, keep shopping.

What usually works and what usually doesn't

What works is being specific and honest. If you sell skincare with active ingredients, say that. If your packaging goes through a co-packer, mention it. If you run regular delivery or seasonal launches that spike inventory, bring it up.

What doesn't work is under-describing the business to get a cheaper quote. That can backfire when you need the policy most.

For founders who want a practical starting point on documentation and operating basics, Loyaltie keeps a useful set of seller materials in its resources hub for brands. It's a good complement to the insurance process because getting insured is easier when your operations are already documented clearly.

Protect Your Passion Your Way

Insurance is easy to frame as a chore. For makers, it's better understood as freedom. It gives you room to pitch wholesale accounts, ship with less anxiety, work with fulfillment partners more confidently, and keep building a brand that people come back to because the products are better and the connection is real.

That matters in a market where people are actively choosing independent brands and local makers. 70% of Gen Z and 69% of Millennials say they're willing to shop locally more often, according to Finance & Commerce's survey coverage. People want to buy directly from the maker. They want the coffee roasted by someone they can name, the skincare made with intention, the pantry staples that don't feel generic.

Your job is to keep that trust intact.

The right e commerce insurance setup does that unobtrusively. It doesn't replace careful labeling, solid fulfillment, or good customer communication. It supports all of them. And when your brand grows, it helps you grow without feeling like one bad week could undo years of work.

If you're ready to sell with more structure, Loyaltie is a marketplace where people discover and buy directly from the best independent brands in the US. It gives makers a straightforward way to reach local buyers online while keeping the relationship direct and the shopping experience simple.