You know the feeling. You ship a great order, the customer is happy, and then your payment statement lands and takes a bite out of the sale that feels way too big. It stings even more when you sell higher-ticket bundles, pantry refills, wellness products, skincare, pet goods, or anything people reorder regularly. You did the hard part. You made something worth buying directly from the maker. Then fees eat into the margin.

For independent brands, that's where ACH starts to matter. Not as finance jargon. As a practical way to keep more of each sale, reduce card-related payment issues, and make repeat buying smoother for customers who already trust you. If you sell online in the US, learning how to accept ACH payments can change how your cash flow feels week to week.

Table of Contents

- Tired of High Fees? Here Is a Better Way to Get Paid

- The savings are real on bigger orders

- The trade-offs are manageable if you plan for them

- Get authorization right first

- Verify the bank account before you pull funds

- Set up your operations before you switch it on

Tired of High Fees? Here Is a Better Way to Get Paid

A lot of makers find ACH the same way. Not from a payments webinar. From a moment of annoyance.

You open your processor dashboard after a strong week of orders, see the fees, and realize the products that should feel most profitable sometimes feel the most expensive to collect payment on. That's especially true when your brand sells refill-friendly goods, curated bundles, or products customers buy on a plan. A loyal customer should be the easiest sale you make, not the one that keeps getting interrupted by expiring cards and retry emails.

ACH gives you another route. Instead of charging a card, you pull payment directly from the customer's bank account with their authorization. In practice, that means lower processing costs, fewer card-related failures, and a cleaner setup for regular delivery.

ACH feels less like a new payment trend and more like finally using the right tool for the kind of business you already run.

If you've been tightening operations, it helps to look at payments as part of accounts receivable, not just checkout. That's why Million Dollar Sellers' AR insights are useful here. The broader point is simple. Collection friction affects cash flow just as much as marketing or fulfillment does.

For a smaller operation, the appeal isn't abstract. It's practical. You keep more of what you earn, your returning buyers get a dependable payment option, and your business becomes less exposed to the usual card issues. If you want a straightforward way to start selling with tools built for direct-to-consumer brands, sell on Loyaltie is one path to explore.

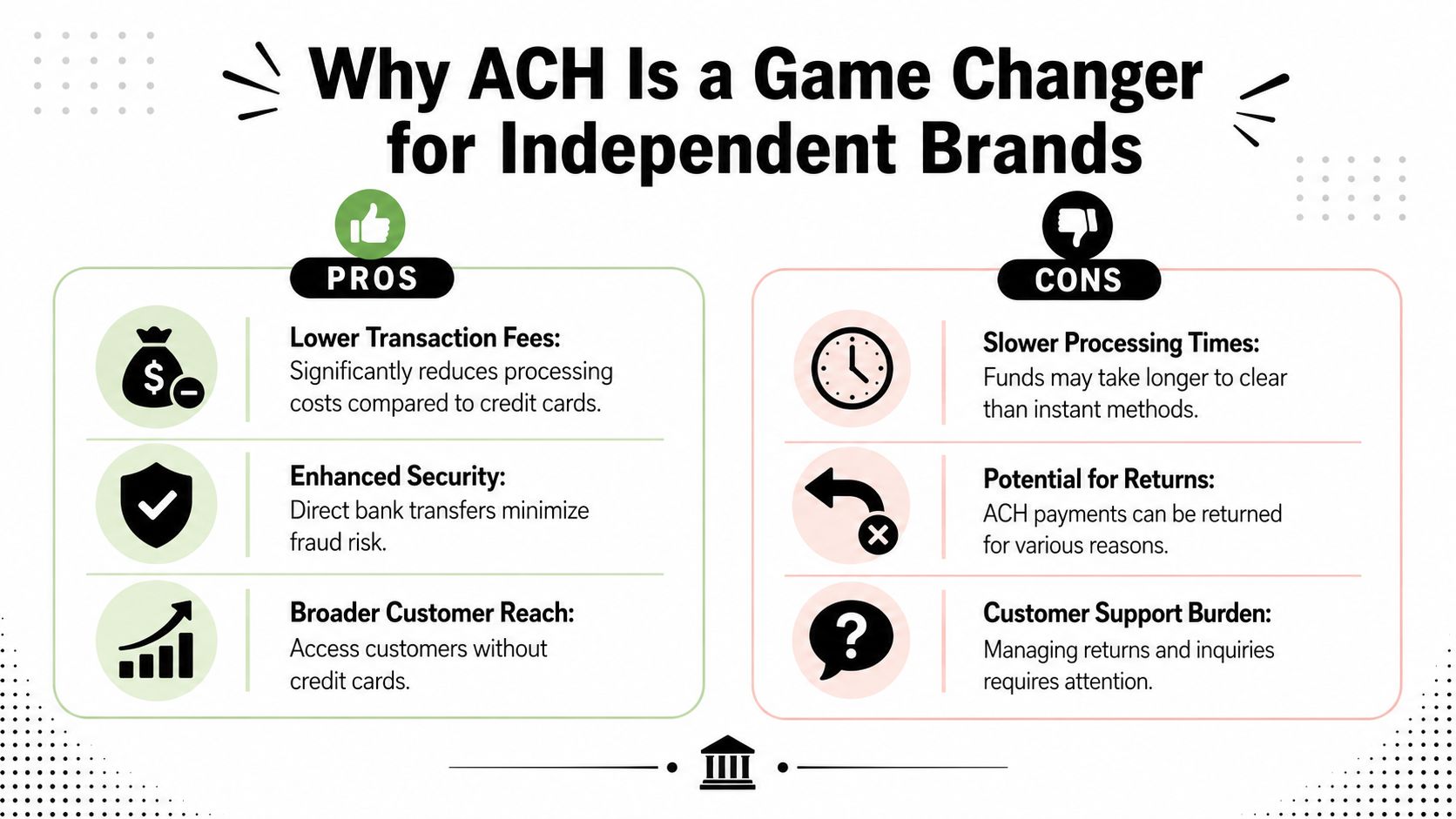

Why ACH Is a Game Changer for Independent Brands

The big reason makers switch attention to ACH is cost. Not branding. Not trends. Cost.

The savings are real on bigger orders

The easiest way to understand ACH is to compare it to a single larger purchase. According to Plaid's ACH payment overview, a $5,000 transaction via ACH can cost a merchant between $0.25 and $5, while the same transaction via credit card can cost between $65 and $175.

That gap matters fast if you sell higher-value products, wholesale-friendly packs, or regular deliveries with a healthy average order size.

Here's the maker version of the math:

| Payment method | Example cost on a $5,000 order |

|---|---|

| ACH | $0.25 to $5 |

| Credit card | $65 to $175 |

For an independent brand, that difference can cover packaging, ingredients, paid acquisition, or stay in the business instead of leaking out with every order.

Plaid also notes that 93% of Americans receive wages via the ACH network, which matters because customers already recognize direct bank transfer as normal behavior in everyday life, not something unfamiliar or sketchy. The same source explains that ACH lets businesses schedule payments up to 60 days in advance, which can help when you're planning inventory, payroll, or regular delivery cycles.

The trade-offs are manageable if you plan for them

ACH isn't magic. It comes with trade-offs, and it's better to be honest about them.

- Funds aren't always instant: Standard ACH usually takes time to settle, so it's not the right fit for every use case.

- Authorization matters: You need clear permission from the customer before you debit their account.

- Returns still happen: A payment can fail if the account details are wrong or the funds aren't there at the moment of withdrawal.

- Support work shifts slightly: Your team may spend less time on expired-card problems and more time answering the occasional bank-payment question.

That said, ACH solves a frustrating problem for brands that rely on repeat purchases. Card payments fail for reasons that have nothing to do with customer intent. Cards expire. Cards get replaced. Limits get hit. Bank-linked payments avoid a lot of that noise.

Practical rule: If your best customers reorder often, payment reliability matters almost as much as conversion rate.

There's also a trust angle. Direct bank transfer can feel clean and deliberate when you explain it well. Buyers who already prefer to buy directly from the maker often appreciate a payment option that cuts out some friction and keeps more of the purchase with the brand instead of the middleman.

ACH won't replace cards for every shopper. It doesn't need to. For many independent brands, it works best as a second option that improves margin on the right orders and makes regular delivery more stable.

Finding the Right ACH Partner for Your Business

Once you decide to accept ACH payments, the next question is who should help you do it.

This choice is less about flashy features and more about fit. You want a partner that matches the way your brand sells, the way your customers buy, and the amount of operational complexity you can realistically manage.

Nacha's ACH payments fact sheet shows why this isn't a fringe payment rail. In 2025, the modern ACH Network safely processed 35.2 billion payments valued at $93 trillion, marking the 13th consecutive year of growth. That tells you two things. Customers recognize it, and providers have had time to build mature tools around it.

Pick for fit, not for features on a sales page

Most makers end up looking at a few kinds of partners:

- All-in-one processors: These can handle card payments and ACH in the same dashboard. That's appealing if you want one reporting flow and one team to contact.

- Bank-linking tools: These focus heavily on connecting and verifying customer accounts cleanly. They can improve the buyer experience during setup.

- Marketplace-based selling setups: If you sell through a marketplace where people discover and buy directly from independent brands, some of the payment complexity may already be handled for you.

The right choice depends on what hurts most today. If checkout ops are already messy, simplicity matters. If your orders are larger and fee sensitivity is high, pricing structure matters more. If you're a one-person shop, support quality matters more than a long list of technical options you'll never touch.

A real-world product example helps. If you sell something like Habanero Salt-Free All-Purpose Seasoning Blend, Garlic & Onion, Everyday No-Sodium Flavor, Net Weight 2.25 ozShaker Bott | DSLW Seasonings by Loyaltie, where buyers may come back for everyday pantry restocks, the customer experience around reordering matters as much as the raw fee number. The product snapshot says it delivers big savory flavor without the sodium, with a bold spicy garlic-and-onion-forward taste that works on chicken and vegetables. That kind of repeat-use product benefits from a payment flow that feels dependable and low-friction.

For makers comparing platforms and operational options, Loyaltie seller resources can help frame the business side of the decision.

What to ask before you sign anything

Don't start with “What's your ACH feature set?” Start here:

- How does pricing work on larger transactions? Flat-fee and capped models feel very different from percentage pricing.

- How is account verification handled? If this is weak, your support workload goes up later.

- What does the authorization flow look like for customers? Clunky consent screens can hurt trust.

- How are returns shown in reporting? You need a clean way to spot and act on failed pulls.

- What kind of support do you get? A fast answer during a payment issue matters more than a polished sales demo.

A good ACH partner should reduce friction, not move it from fees into customer support.

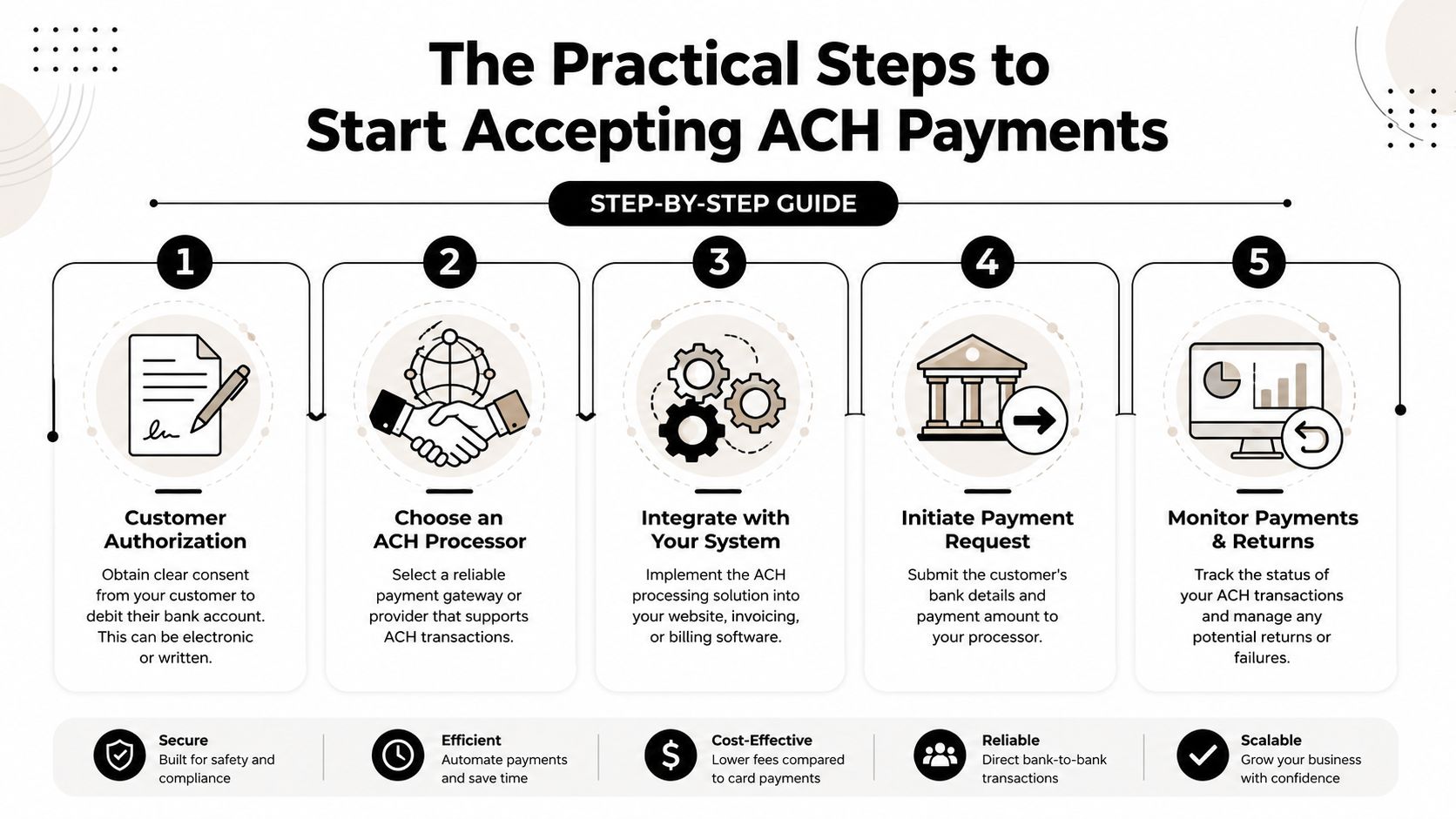

The Practical Steps to Start Accepting ACH Payments

A customer is ready to place a larger reorder, sees the bank payment option, and pauses for one reason. They want to know it will work the first time and that they will not have to chase your support inbox later. That is the primary setup job with ACH. The technical connection matters, but the customer-facing details decide whether ACH saves you money or creates cleanup work.

Nacha's consumer payment rules make one point clear. You need proper authorization before you debit an account, and you need to retain proof of that authorization. For an independent brand, that means building a checkout or invoice flow that is easy to understand, easy to document, and easy to find later if a customer has a question.

Get authorization right first

Start here, because weak authorization turns a low-fee payment method into a customer service problem.

Your authorization can be digital or written, but it should clearly state what the customer is agreeing to. Include the account holder's name, the payment amount or how it will be calculated, whether it is one-time or recurring, the timing, and the date they approved it. Keep a record that ties the authorization to the order.

A bare minimum statement like this is too thin:

I authorize [business] to debit my account.

Use plain language that matches the actual purchase. If you sell direct to customers, especially repeat-purchase products, the buyer should be able to read the authorization and immediately connect it to the order in front of them. That clarity helps with trust and with reducing dispute rates, because confused customers are more likely to challenge a payment even when they meant to buy.

A solid authorization flow usually includes:

- Clear timing: Say when the debit will happen.

- Specific order details: Reference the product, invoice, subscription, or reorder.

- A confirmation record: Email the customer a copy they can keep.

- Visible consent: Use an unchecked box, signature field, or similar action that shows clear approval.

Later in the process, this explainer is worth watching if you want a visual walkthrough of ACH basics:

Verify the bank account before you pull funds

Manual entry works. It also creates avoidable mistakes.

If customers type in routing and account numbers by hand, some payments will fail for simple reasons: a typo, a closed account, or an account that does not belong to the person checking out. The Federal Reserve explains in its ACH overview that ACH payments move through a batch network rather than instant card rails, so errors often show up after you have already treated the order as paid. That delay is why account verification matters so much for smaller brands with tight cash flow.

Good ACH setups use bank-linking or verification tools to confirm the account details before the debit starts. That cuts down on failed payments and gives buyers a cleaner checkout experience than making them hunt for bank numbers and enter them manually.

For marketplace sellers, including shops on Loyaltie, this matters even more on reorders. A buyer who already trusts your product should not hit friction on the payment step.

Set up your operations before you switch it on

The banking setup itself is simple. The operational decisions are where brands usually get sloppy.

Connect ACH to your business bank account, not a personal account. Decide where customers will see it, such as checkout, invoice links, or reorder reminders. Then decide which orders should use ACH first. Many small brands start with higher-ticket orders, wholesale-style invoices, or repeat buyers because those cases usually justify the extra setup and customer education.

Use this rollout checklist:

- Connect the right bank account: Keep business funds and reconciliation in one place.

- Choose the first use case: Checkout, invoices, subscriptions, or reorder campaigns.

- Set customer eligibility rules: New buyers and repeat buyers do not always need the same payment options.

- Write the support copy now: Prepare the email or help reply for pending payments, failed debits, and customer questions.

- Run your own test payment: Check the confirmation email, reporting, and payout visibility before customers touch it.

The practical order is simple:

- Connect your business bank account.

- Choose your ACH provider.

- Build the authorization form or checkout step.

- Turn on account verification.

- Test a small internal transaction.

- Review what the customer sees after payment, including receipts and support messaging.

That order prevents a common mistake. Brands turn on ACH because the fees look better than cards, then realize the post-purchase experience is vague, the reporting is messy, and support has no script when a buyer asks why the payment still shows as pending. For a small operation, getting those details right is what makes ACH worth offering.

Managing Payouts Returns and Customer Questions

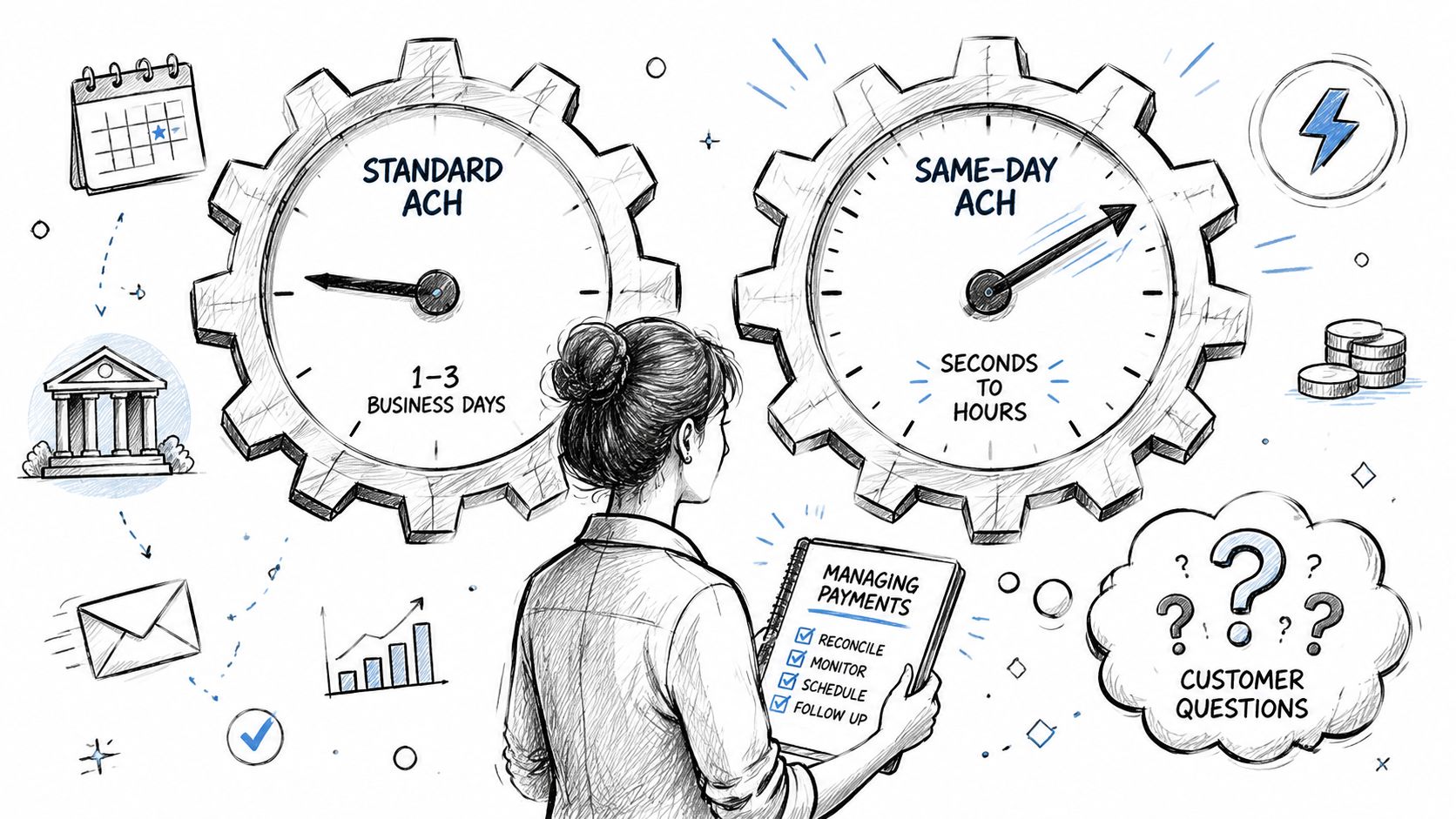

A customer places a $140 order on Monday morning, and your bank payment shows as pending. By Monday afternoon, you are deciding whether to ship now, wait for cleaner payment status, or risk eating the cost if the debit comes back unpaid. That is the part of ACH that matters for a small brand. Not the acronym. The timing.

What payout timing feels like in real life

ACH can be cheaper than cards, but it does not behave like card money. Funds are not always available right away, and returns can still hit after the order is placed. For an independent brand, that changes fulfillment decisions fast.

The practical rule is simple. Match your shipping speed to your risk.

If you sell made-to-order products, personalized goods, or anything hard to resell, waiting for a cleaner payment status can save you from avoidable losses. If you sell lower-risk items to repeat buyers, you may choose to release orders sooner because the customer history lowers the chance of trouble.

Same Day ACH can help when speed matters, but it costs more than standard ACH. Nacha explains that Same Day ACH is available for faster processing windows, while standard ACH follows the regular batch schedule through the network. Use faster processing for situations where quicker access to funds or faster order release demonstrably changes the outcome, not as your default for every order. The official ACH Network resources from Nacha are a better reference for timing expectations than a provider sales page.

For brands selling through a direct-to-consumer storefront or a marketplace for independent brands, this matters most on higher-ticket orders. A delayed payout on one small accessory sale is annoying. A return on a $300 custom bundle is a margin problem.

How to handle failed payments without damaging trust

Failed ACH payments usually come from ordinary issues. The account number was entered wrong. The balance was too low on debit day. The customer does not recognize the payment description. A bank flags the transaction and stops it.

Nacha publishes standard ACH return reason codes, and they are worth reviewing because they help you separate fraud concerns from normal payment problems. If you know the difference between insufficient funds, invalid account details, and an authorization issue, your team can send the right response instead of a vague apology. The ACH return code reference from Nacha is useful for that.

What customers need is clarity.

A good message sounds like this:

We could not complete your bank payment for order [number]. Your order is on hold for now. If you want, we can help you retry the bank payment or switch to another payment method.

That tone protects the relationship. It also gets more payments recovered because the buyer knows what happened and what to do next.

Refunds need the same level of clarity. Tell customers that the refund is being sent back through the original bank payment method, and tell them the bank posting time can vary. Then send a written confirmation so they are not left checking their account and guessing.

If you want fewer support tickets, build your process around recognizable descriptors, clear authorization language, and short status updates before the customer has to ask. The same habits that help with reducing dispute rates also help here. Customers stay calmer when the payment activity makes sense the first time they see it.

The brands that handle ACH well are usually boring in the best way. They review pending payments daily, flag risky orders before fulfillment, keep refund language plain, and save support replies for the few questions that come up again and again. That is what keeps ACH savings from getting eaten by manual cleanup.

A Simpler Path for Makers on Loyaltie

A lot of makers read through ACH setup details and reach the same conclusion. The payment method makes sense. The admin work sounds less fun.

That's fair. If you run an independent brand, your best hours are probably spent improving your product, talking to customers, shipping orders, and planning your next release. Not building authorization flows or chasing return codes.

Marketplaces can make a lot of sense. Instead of setting up every part of the payment stack yourself, you sell inside an environment where the payment experience is already structured for direct-to-consumer buying. That doesn't remove every operational responsibility, but it can remove a lot of the setup burden that keeps makers from offering better payment options in the first place.

For brands that want discoverability and a simpler path to selling online, Loyaltie is a marketplace where people discover and buy directly from the best independent brands in the US. For a maker, that means you can focus more on the product and the customer relationship, while the platform handles more of the commerce plumbing behind the scenes.

That marketplace model also fits how many shoppers already want to buy. They're not just looking for another mass-produced option. They want better everyday products from real people, with no middleman when possible. Survey data cited by Finance & Commerce found that 70% of Gen Z and 69% of Millennials are willing to shop locally more often, and consumers said they were willing to spend nearly $2,000 more in 2024 if it meant their favorite local shops would continue to thrive. For makers, that signals real appetite for buying from independent brands.

If you also need help creating content that makes your products easier to discover and trust, platforms like JoinBrands can be part of the mix. Good product storytelling and clean payment experiences work well together.

The point isn't that every maker should build a custom ACH system. It's that you should choose the simplest route that gives your buyers a smooth experience and gives your business healthier margins.

If you want a simpler way to reach customers who prefer buying directly from the maker, Loyaltie offers a marketplace where people discover and buy from independent brands across the US, with a built-in commerce experience that helps you spend less time on payment setup and more time on the products people come back for.